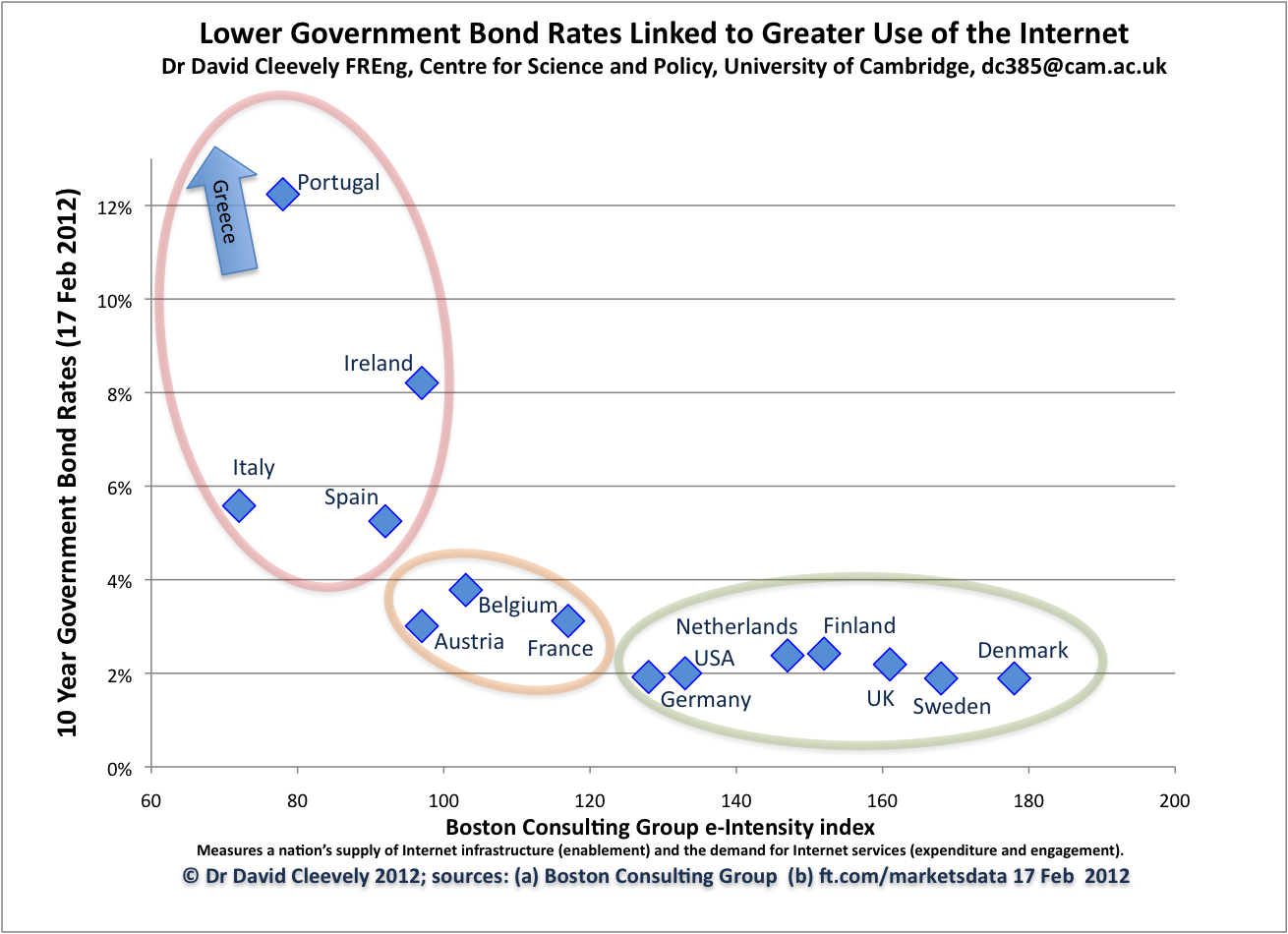

This snapshot of a handful of countries

post-economic crisis shows one thing very clearly: a country’s ability to weather the economic crisis is related strongly

to its level of modernisation or e-Intensity.

Note: e-intensity is a measure developed

by the Boston Consulting Group based on adoption, expenditure and use of the

internet and e-commerce. Our analysis puts e-intensity against 10 year

government bond rates as our measure of how well a country is weathering the

economic crisis.

The results of our simple analysis are particularly

striking within the Eurozone. Member states which have not had the capacity to

adopt and develop the internet and ecommerce are those with skyrocketing risk

premiums on their governments’ debt. These states form a distinct group:

Portugal, Italy, Spain, Ireland and Greece (which is literally off the scale) -

all with high debt premiums and an e-Intensity score of well under 100.

There are two other groups: those with high

e-Intensity and low government bond rates such as Germany, Denmark and the UK,

and a middle group (Belgium, Austria and France) with lower e-Intensity

(100-120) and raised bond rates of 3-4%.

So why is there such a close relationship?

There are two possible explanations, and both could be correct:

a) Low e-Intensity indicates underlying

structural problems: countries with high e-Intensity are those which have

invested in modern processes, improved productivity and benefit from strong

institutions. These are the countries that have lower borrowing costs, as they

are best placed to grow their economies in the future.

b) e-Intensity (or what it represents) is a

fundamental capability: countries which use the internet intensively can

respond more flexibly to shocks and crises, instead of being weighed down by

cumbersome 20th century processes and institutions.

What makes these two explanations

compelling is the following: if you can get a country to invest in, use, and

compete on the internet, then you must have either eliminated or minimised any underlying

structural problems, or created a flexible and robust economy, or both.

Five of the countries shown here (Greece,

Portugal, Ireland, Spain and Italy) have been slow to embrace new technology,

business models, and to change consumer behaviour. Much has been written about

the institutional problems these countries face, but we think a very specific

problem might lie at the heart of the current economic crisis: how do you get

these countries to invest in and use the internet? And both investment and use

are necessary – just buying infrastructure and fancy web sites won’t cut it.

Our questions:

1. Is the internet a line in the sand for Europe?

Does a country’s ability to adopt and exploit modern technologies dictate whether

it can operate within the single currency?

2. Can the problem be addressed in time?

Does this highlight a structural issue that takes decades to solve, or is it a

faster acting killer-policy-app for the Eurozone’s troubled economies that

could keep them in the single currency for good?

3. Should investment in e-Infrastructure and

stimulation of usage become a policy priority for Europe?

We will answer question 3: “Yes,

immediately”. Of course, further evidence is needed and linkages need to be

demonstrated, but the risks are high and the expensive parts of the solution -

infrastructure investment - can have well-calculated returns.

Whatever the underlying mechanisms, it is

clear that the internet is playing a very significant role in modern economies,

and one which may extend far beyond its direct share of GDP.

About the Authors of this post:

David Cleevely is Founding Director of the Centre for Science

and Policy at the University of Cambridge.

Matthew Cleevely is an entrepreneur pursuing a PhD in

entrepreneurship, innovation and growth policy at Imperial College Business

School, London

The BostonConsulting Group e-Intensity Index (BCG Perspectives) used in this

analysis compares different measures of Internet activity for 50 countries. It

measures the three significant factors:

i.

Enablement. How well built is the

infrastructure and how available is access? (This has a weighting of 50

percent.)

ii.

Expenditure. How much money is spent on online

retail and online advertising? (25 percent.)

iii.

Engagement. How actively are businesses,

governments, and consumers embracing the Internet? (25 percent.)